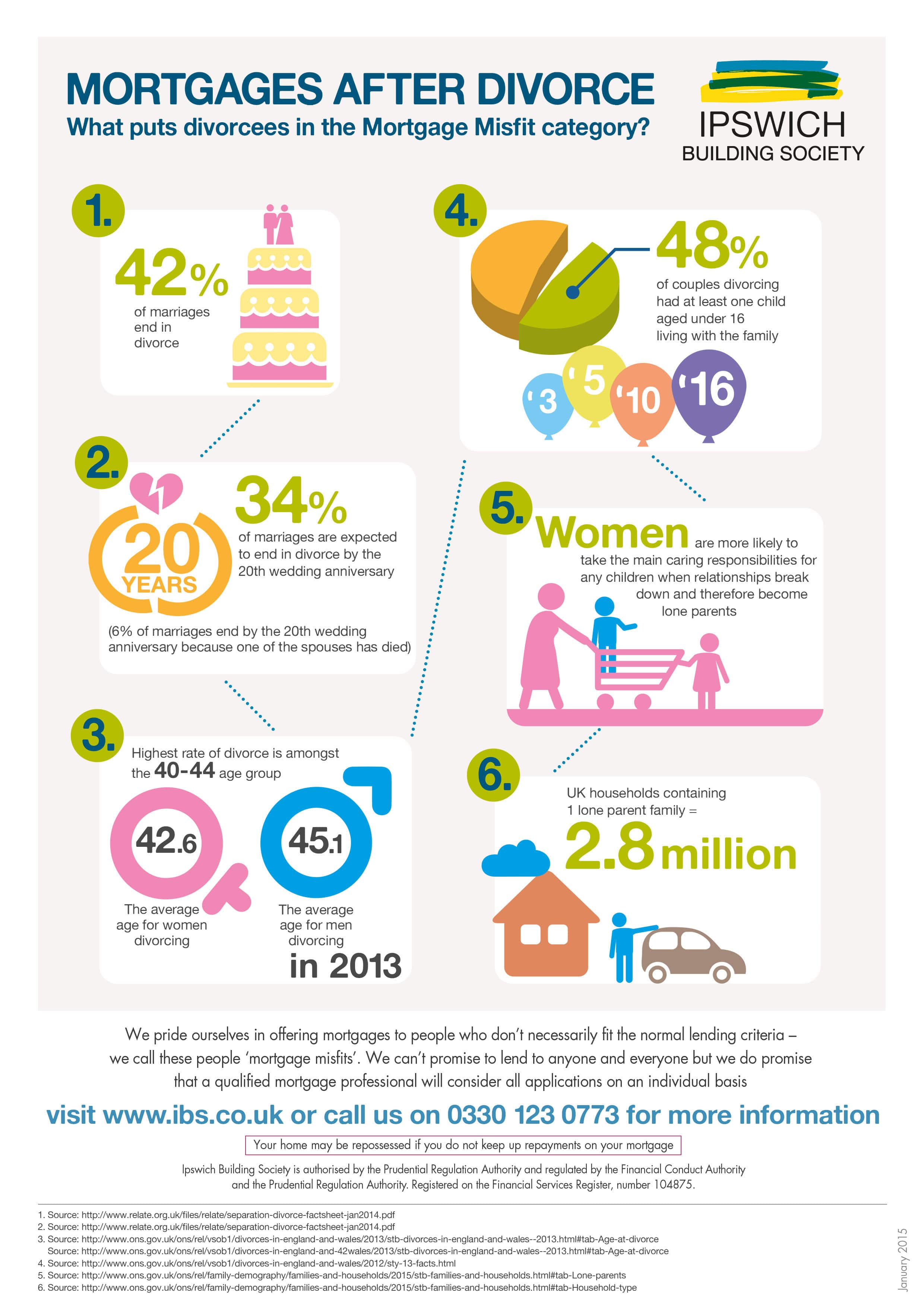

Thanks to the Mortgage Market Review (MMR) bringing in stricter affordability criteria for those looking to buy a home, specific groups of people finding it harder and harder to get a mortgage. People looking for a mortgage after divorce are the latest group to join these so called ‘mortgage misfits’.

Whilst these ‘mortgage misfit’ divorcees may be able to afford the mortgage in reality, due to a variety of income channels, the computer based affordability tests used by many lenders automatically assumes they cannot afford the repayments because they do not recognise child maintenance as income. Our infographic below illustrates why this is a big problem for a growing mortgage misfits group.

Suffolk Building Society is one of the only lenders that takes into account 100% of child maintenance payments and will also consider an applicant’s evidence if they routinely spend less than the national average on specific items, offering greater choice of mortgage products to divorcees and lone parent households.